When I first became interested in the idea of pro-active business management in the mid 1970’s the prevailing sentiment at the time was that you had to be tighter, tougher, leaner, meaner or die. Being youthful and mentally aggressive I was seduced by this notion. Fortunately, I was teaching at the time so I didn’t have much opportunity to let myself loose on an unsuspecting business community.

Towards the end of the 1970’s I did start to do some work with business people. Specifically, I started playing with the application of non-financial measures of performance. I had come across a book written by John Humble called Improving Business Results and it was the first time I heard the term Key Results Analysis used. Humble’s idea was that business activities can be defined in terms of Key Tasks with associated Performance Standards and Controls used to measure performance.

What initially appealed to me about Humble’s thesis was that it was totally consistent with research I’d been doing on monitoring idle capacity. But then I was hit by a blinding flash of the obvious as soon as I read the following sentence:

“In this column are listed the small number of tasks which will have a major impact on success” (emphasis added)

I was very much aware that small business people can’t comprehend the significance of traditional accounting reports and in any event they are usually too late in coming. However, small business people do understand the activity end of their business. It seemed to me quite logical that accountants could apply their obvious skill in measurement to the task of firstly identifying the few key activities that are critical to success. They could then put in place a system for reporting on how the business is going, literally daily, in relation to these activities.

One of my students in the Small Business Program I was teaching owned a retail business. After a lecture on Key Results Analysis he came up and said he was going to have a go at this. So we selected the number of sales, the average value of a sale and the GM% (measured as a weighted average of the weekly sales mix) as the Key Performance Indicators. We carefully selected weekly and daily targets and tied everything back to an annual profit plan. The idea was, that he would know at the end of each day whether he was on line to make his annual profit target which we’d ambitiously set at 25% above his previous best year.

Nothing changed however. For two months we measured and monitored. I was about to eat Humble Pie when another thought occurred to me. The mere act of measurement does not in and of itself change the object of measurement. If you want to change the object you have to take some sort of action. So the question arose, what are we measuring and how can we change it? When we thought about it we were actually measuring four things not three: they were price, the number of items per transaction, the number of transactions and the GM%.

Having analyzed what we were measuring we then said: what can we do to change these in our favor. To favorably change price, you increase it – we couldn’t do that, we’d lose sales. Let’s do a few more calculations to calculate how much our sales would have to fall before we’re worse off. The results are the two tables in my booklet ‘What You Can Do to Improve the Profitability of Your Business’. That was enough for Graeme to give it a go on a few items – we did that, measured the result and discovered something profoundly interesting: volume doesn’t necessarily fall when you raise price. So we changed the price of a few more items.

We also looked at what seemed to be a more difficult task, namely to do something to change the number of items per transaction and the number of transactions per day. To try and increase the items per transaction we fiddled with things like changing the location of impulsive lines on the counter and discounted product display bins – they had a bit of an effect but nothing to get excited about. Then Graeme came up with the idea that he’d relocate a high customer traffic department to the back of the shop. That way people would have to spend more time in the shop and walk past more goodies. It worked, sales jumped.

Then we figured that we’d sell more items per transaction if the sales people stopped asking “is that all” and started, what I now know to be called, companion selling e.g. if someone purchased a product for which there was a logical companion product the sales people would politely remind the customer not to forget the <Whatever>, and time permitting, would take the customer to the display area. That also seemed to work because sales per transaction steadily climbed as did the average value.

We stumbled on the next idea. It happened at a team Christmas Party. I was fortunate enough to be invited – I think it was my fee actually. Anyway one of the team asked why we’d been changing everything around and why we were preoccupied with all this key performance stuff. Graeme explained the theory of the whole thing – the story about how accounting reports don’t help you manage a business because they are too aggregated and too late in coming and that what we’re experimenting with is ways to increase unit sales etc.

Then one of the team said that makes sense and what we should do is set shop targets for each of the things being measured and every time a record is broken everyone would get a prize of some sort. I had again been Humbled, first by John and now by Michael. Involve the team was the message. The team are at the coal face; they are the people who control the activity. Give them something to shoot for. Give them involvement. Trust their judgement.

In the final analysis you’ll be the judge as to whether this stuff works. But I’ve seen it work in fabrication shops, gift stores, menswear, accounting practices, service stations, bike shops, hairdressers, painters, plumbers, kitchen manufacturers, motels, restaurants and coffee shops… and I’ve seen it fail in those businesses – it’s the execution not the concept that’s the key.

And the secret is:

- select something that represents a key activity in the business

- break it down into its absolutely lowest common denominator

- ask yourself how it can be changed by a decision or action from every conceivable angle

- measure the result of any change that is made – make one change at a time

- involve your team in the process

- invite them to contribute ideas about what can be changed and how feedback the results to them regularly and with passion

- have fun

- buy a cornsack to do your banking

And that brings me to the early 1980’s when I decided to peddle these ideas from the platform of a public practice. I was in for another series of lessons, the most important of which was that it’s a lot easier to make a business perform better than it is to convince the clients that it’s possible and that we can help them do it.

By this time, I had come to the conclusion that the proposition that a business needed to be a lean, mean, fighting machine was fundamentally flawed.

What a successful business needs to be, in my view, is a focused, flexible, observant, responsive, experimental, trusting, personal, willing, learning organization. And most importantly, there needs to be a simple system for communicating to everyone in the organization exactly how they and the business are performing. It needs a leader with a vision that makes sense and which is understood by everyone.

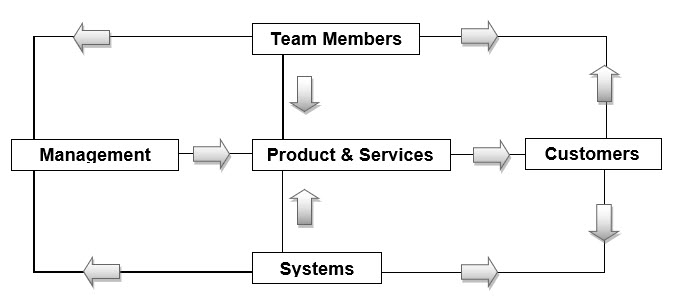

The business model that drives the consulting work I do is illustrated in the diagram below.

This model shows the business as an organization of continuous interaction. Management determines what the business does for its market and therefore defines the products and services that will be offered having regard to the discovered needs of customers. Management then creates an environment in which team members and systems can interact to produce the output of the business.

Customers interact with the products and services in the sense that they use, enjoy or avail themselves of the output. But they also interact with team members and with the systems. It is the experience with the team members, the products and the systems, that determines customers’ ultimate assessment of value and their final vote as to the future of the business.

In response to this customer assessment, management adds value to the key resources of the business: its people and the systems it uses to create value, with the goal being to create an experience for the customer, that is both valued and sought.

The strategies that emerge from this way of looking at a business are:

- develop managerial clarity of purpose and focus

- develop team member commitment and responsive capability

- develop efficient and customer-sensitive systems

So that you:

- produce a product or service consumption experience that delight customers.